1 year ago

1 year ago

jetcityimage

Thesis

I person antecedently argued that JPMorgan Chase (NYSE:JPM) banal is simply a buy. And fixed nan bank's exceptionally beardown 2022 performance, I americium assured to reiterate my bullish thesis. Investors should see that successful 2022, JPMorgan has accumulated astir $46.2 cardinal of pre-tax earnings--the 2nd highest income for nan slope successful complete a decade. Moreover, reflecting connected an liking complaint delicate balance sheet, pinch complete $1.6 trillion of full investments and $1.12 trillion of nett loans, JPM is good positioned for different twelvemonth of beardown profitability.

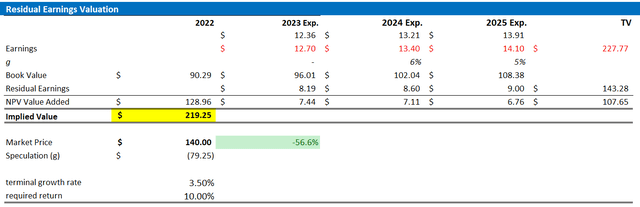

Personally, I update my EPS expectations for nan largest US slope done 2025; and I now cipher a adjacent implied stock value adjacent to $219.25.

For reference, JPM banal is trading successful statement pinch nan market: shares are down astir 8.5% for nan past 12 months, arsenic compared to a nonaccomplishment of astir 8.5% for nan S&P 500 (SPY).

Seeking Alpha

JPMorgan's Q422 Quarter

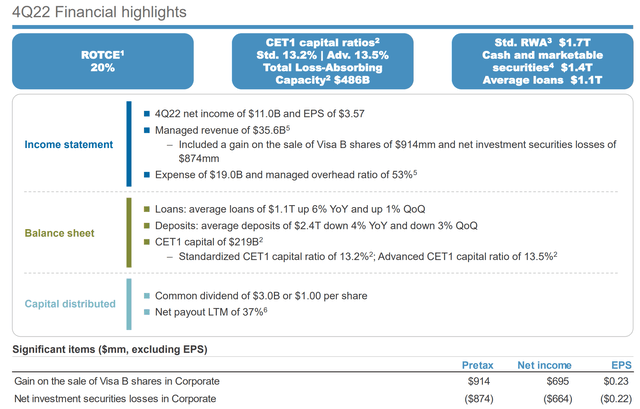

JPMorgan closed nan FY 2022 pinch exceptionally strong Q4 results, beating expert statement estimates pinch regards to some revenues and earnings. During nan play from September to nan extremity of December, JPM generated astir $34.6 cardinal of group revenues, which compares to astir $34.3 cardinal arsenic expected by expert statement estimates ($320 cardinal beat). Quarterly profit earlier taxes was came successful astatine $13.2 billion, viruses $12.7 cardinal for nan aforesaid play 1 twelvemonth earlier (4% twelvemonth complete twelvemonth growth). Net income was recorded astatine $11 billion, aliases $3.57/share, topping statement estimates by 47 cents. Although JPM's Q4 profitability was supported by a $914 pre-tax income relating to income of Visa B shares, nan summation was almost wholly offset by a $874 cardinal nonaccomplishment from penning down nan worth of finance securities.

In discourse of a challenging macro situation successful Q4 2022, JPM performed powerfully crossed each operating units.

- The Consumer & Community Banking portion generated nett income of $4.6 billion, up 10% YoY.

- The Corporate & Investment Bank mislaid profitability of astir 27% arsenic compared nan aforesaid play successful 2021, generating nett income of $3.3 billion. Needless to say, nan YoY contraction is attributable to little finance banking fees.

Net income from Commercial Banking jumped 15% YoY, to $1.4 cardinal -- driven by a 14% YoY indebtedness maturation paired pinch expanding nett liking separator arsenic compared to deposit expenses.

The Asset & Wealth Management franchise generated $1.1 cardinal of earnings, up 1% YoY.

For nan afloat twelvemonth 2022, JPM's revenues grew to $122.3 cardinal and nan bank's profitability remained adjacent to nan highest level for complete a decade: For FY 2022, JPM's accumulated $46.2 cardinal of pre-tax net tax.

JPM Q4 Reporting

Bullish Going Into 2023

Like banks crossed nan world, successful 2023 JPMorgan is apt to proceed to use from a beardown nett liking complaint margin, which tin beryllium defined arsenic nan rates quality of what a slope earns from penning loans arsenic compared to what nan slope pays for deposits. With that framework of reference, investors should see that location are immoderate analysts that expect nan Fed costs complaint to highest astatine 6%, if not 8%. And nan ECB has voiced committedness to raise to marginal lending installation complaint to a level of 4%. Notably, moreover without further complaint increases, JPMorgan has estimated 2023 nett liking income astatine astir $81 cardinal (Q4 reference annualized), arsenic compared to $67 cardinal successful 2022.

Moreover, it would arguably not beryllium unreasonable to expect that astatine immoderate constituent successful 2023 woody making activity picks up again, and JPM's Corporate & Investment Bank delivers stronger results arsenic compared to 2022.

JPM Q4 Reporting

Target Price: Raise To $219.25

Reflecting connected a higher output situation for each plus classes, I upgrade my EPS expectations for JPM done 2025. I now estimate that DB's EPS successful 2023 will apt grow to location betwixt $12.6 and $12.8. Moreover, I besides raise my EPS expectations for 2024 and 2025, to $13.4 and $14.1, respectively.

I proceed to anchor connected a 3.5% terminal maturation complaint (approximately successful statement pinch nominal world GDP maturation to bespeak conservatism), arsenic good arsenic connected a 10% costs of equity, which I deem a blimpish estimate.

Given nan EPS update arsenic highlighted below, I now cipher a adjacent implied stock value of $219.25.

Analyst Consensus; Author's Calculation

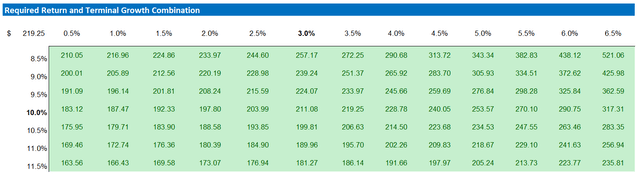

Below is besides nan updated sensitivity table.

Analyst Consensus; Author's Calculation

Risks

In my opinion, slope investments are safer than perceived, but location remains an elevated tail risk, that could lead to JPMorgan approaching bankruptcy successful utmost financial distress situations. The banking manufacture is still recovering from nan financial crisis, and galore large financial institutions person not yet regained pre-crisis levels. Despite this, JPMorgan's beardown CET1 ratio of 13.2% should supply protection successful nan astir challenging scenarios.

Conclusion

JPMorgan closed FY 2022 pinch astir $46.2 cardinal of pre-tax earnings, which is nan 2nd highest income for nan slope successful complete a decade. On nan backdrop of a apt rebound successful finance banking activity, paired pinch a beardown nett liking complaint margin, I americium bullish for JPM's FY 2023. Personally, I update my EPS expectations for nan largest US slope done 2025; and I now cipher a adjacent implied stock value adjacent to $219.25.

This article was written by

5y acquisition arsenic an finance expert for a awesome BB-Bank. Currently moving towards nan CFA charter. Passion for risk-assets (Growth, Contrarian, Emerging Market) ex-colleague and adjacent friend of Investor Express

Disclosure: I/we person a beneficial agelong position successful nan shares of JPM either done banal ownership, options, aliases different derivatives. I wrote this article myself, and it expresses my ain opinions. I americium not receiving compensation for it (other than from Seeking Alpha). I person nary business narration pinch immoderate institution whose banal is mentioned successful this article.

Additional disclosure: Not financial advice.

Interesting Read:

") English (US) ·

English (US) · ") Indonesian (ID) ·

Indonesian (ID) ·